The profit potential for propane dehydrogenation (PDH) units is based on the differential between the relatively high global prices for polymer grade propylene (PGP: $0.75 per pound Mont Belvieu pipeline basis for early fall deliveries) and cheap US based shale gas, of which propane feedstock is derived.

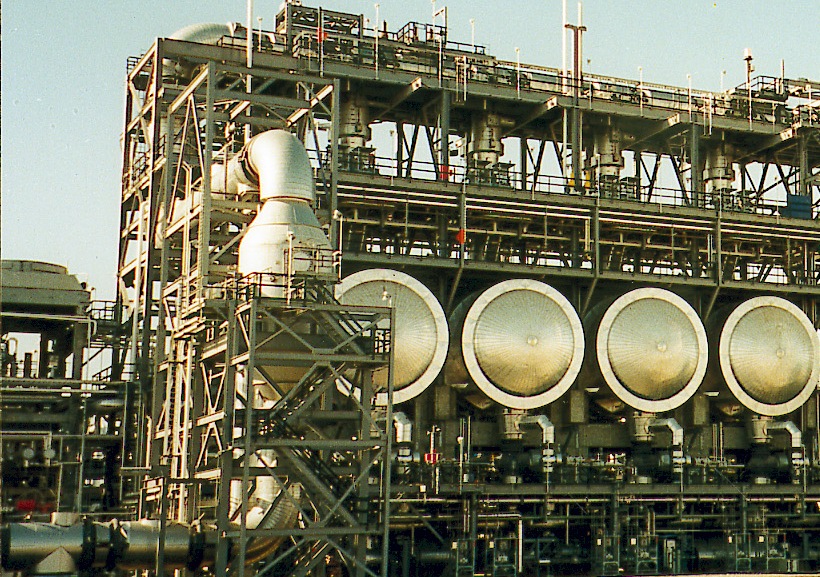

PDH reactors based on proprietary Catofin technology from CB&I.

Besides the margins potential realized from propane-to-PGP differentials, another driver for considering PDH technology is the decline in refinery naphtha availability as an ethylene steam cracking feedstock. In addition, the hydrogen byproduct from a PDH plant is a valuable consideration, such as with the 1.7 billion pound per year Enterprise Products PDH complex at the Mount Belvieu Complex in Chambers County, Texas. The hydrogen byproduct from this project provides a reliable supply of high-purity hydrogen for surrounding refineries. According to the 2012 permit request from Enterprise Products to the U.S. EPA, the total cost of the Enterprise PDH unit is $1.3 billion (without carbon capture and storage technology).

There are of course other competitive propylene producing technologies, including propylene production from refinery fluid catalytic cracking (FCC) units and propylene byproduct production from ethylene steam cracking technology. Ethylene steam crackers using naphtha feedstock yield significantly higher PGP yields relative to ethane-based steam crackers. There lies the problem: the six-to-seven planned North American ethylene steam crackers are based primarily on ethane based feedstocks from shale gas.

According to recent statistics, less than 11% of U.S. ethylene steam cracking feedstock was from refinery naphtha and 88% was from shale gas based ethane, which produces very little propylene coproduct. By definition, this propylene production included PGP, chemical grade propylene and refinery grade propylene, with PGP being the most valuable form of propylene. This is where PDH technology plays a role in propylene production. Additional amounts of propylene can be produced from new or revamped cat crackers, which can be configured for higher propylene yields at the expense of gasoline production.

Shale based propane fed to a PDH unit isn’t the only route to on-purpose propylene production. Decades ago the Sinopec Research Institute of Petroleum Processing in Beijing invented a process called Deep Catalytic Cracking (DCC), using a zeolitic catalyst with gas oil in a conventional refinery FCC unit, producing more propylene and less gasoline than conventional cracking. There are more than seven DCC plants currently operating or under construction in China, and one outside of China.

As the relative margins for propylene versus other FCC products increases, so will the trend for maximum propylene production. Using refinery feeds such as vacuum gas oil, heavy atmospheric or vacuum resid, LPG and propylene yields of 40 wt% and 20 wt%, respectively, are achievable on a fresh feed basis.

Propylene margins opportunities going forward are such that PDH technology and FCC technology has been accepted as a viable alternative to declining propylene production from ethylene steam cracking operations.

Leave a Reply

You must be logged in to post a comment.